Sean Gallup

Stocks that are leveraged to financial toughness in one way or a different have been wrecked this year. When you pair that with stocks that prosper in very low-price environments, you get a certainly horrendous ideal storm. Which is how perennial industry leaders like Alphabet (NASDAQ:GOOG) stop up shedding a 3rd of their worth, which is just what took place previously this year.

Alphabet has offered off with the rest of the marketing shares such as Snap (SNAP), Meta (META), Pinterest (PINS), and so on. Certainly, the problems has been much additional significant with those people names, but that is due to the fact they don’t operate a monopoly in 1 of the world’s largest organization, which Alphabet enjoys with Google. As Alphabet was dragged down – unfairly in my look at – and the truth that net shares are now back again in favor on Wall Road, Alphabet is a screaming acquire.

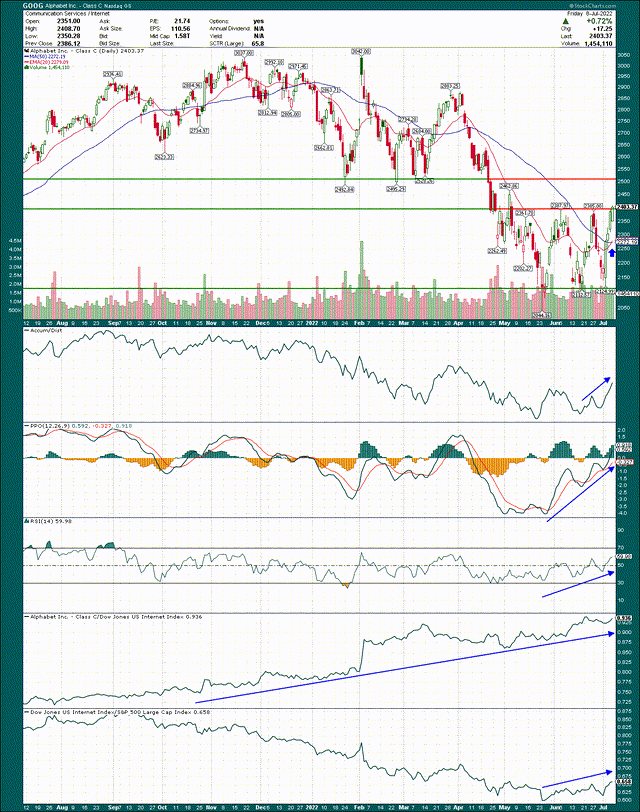

Let’s start out with the chart, which exhibits a sizable consolidation that Alphabet is heading to crack this 7 days, or really shortly thereafter.

StockCharts

I’ve drawn in the strains for the consolidation and they correspond about to $2,100 and $2,400. All those are your strains in the sand when it comes to buying and selling all around the consolidation, but in this scenario, I think Alphabet has consolidated sufficient that you just want to maintain it, alternatively than danger missing the massive go to the upside.

The motive is due to the fact all of the indicators glimpse fantastic at this position for the bulls. The accumulation/distribution line has turned sharply better, indicating major money is obtaining dips fairly than advertising rips.

The PPO has exploded greater, indicating not only vendor exhaustion, but outright bullish momentum. This is the type of issue we see at key bottoms, which generally direct to sustainable rallies. The 14-day RSI is displaying the very same thing.

Alphabet has outperformed its friends for a long time, which surprises no 1. But importantly, world wide web shares are lastly getting some ground on the broader marketplace, which has not been the situation for some time. Although internet stocks are considerably from a primary team suitable now, I believe the possibility is there for them to turn into just that, and Alphabet is a demonstrated winner in the group.

At last, potentially just one of the most bullish points on this chart is the simple fact that the 20-working day EMA has just crossed more than the 50-working day SMA. This comes about when the craze has transformed, and we know that it happened quite a few months back when the inventory topped out. The reverse is happening now, and these lines should develop into help on the way up, just as they have been resistance on the way down.

Provided the momentum we’re looking at, I imagine the odds of Alphabet breaking out sooner than later on are pretty significant, but even if this 1 is turned down this week, get Alphabet on the pullback at the 20-working day EMA.

Let’s now acquire a seem at the elementary scenario for Alphabet to see if it is a lot more than just a bottoming inventory.

Recession agony priced in

We all know about Alphabet’s corporations, which incorporate lookup, YouTube, Cloud, Network, and its enterprise cash fund Other Bets. The Research company is by much the premier by no matter what metric you want to use, and it’s also the a person that is reliant on businesses seeking to devote money promotion. That is why the inventory fell so sharply into the center of 2022, but as we know, the Research enterprise is basically a monopoly, and specified that, it’s so huge that it is not as cyclical as other advertising and marketing platforms. That is why Alphabet shares have not fallen almost to the extent other advertising and marketing stocks have, and why there is significant upside from in this article.

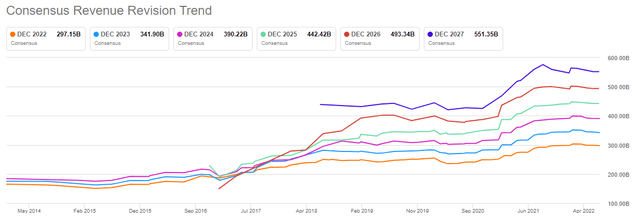

Trying to get Alpha, revenue revisions

We can see with income revisions that analysts have made downgrades for many months, but there are two critical factors I want to make. First, revisions downward are extremely compact in magnitude, and absolutely nothing like the ~30% decrease in the share cost we saw. Second, they’ve flattened out in current months, as you’d assume provided that a economic downturn is generally priced in prior to it comes. The upside of this is that now that estimates are decrease, which means sentiment is weaker, and that estimates have flattened out, it would consider a new shock to transfer them meaningfully decrease yet again. That means the route of least resistance is increased, and that is exactly when we want to acquire the inventory.

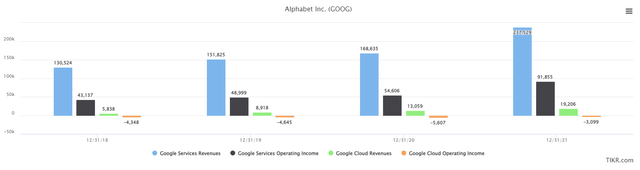

Hold in head also that Alphabet has grown its advertisement enterprise by all forms of headwinds prior to, all of which appeared a lot even worse than the present-day ecosystem. These include things like the “ad-pocalypse” from 2020 and 2021 following COVID lockdowns, where by advertisement expending fell off a cliff in unprecedented trend. But you wouldn’t know it by looking at the below.

This is once-a-year profits by segment for Google Solutions and Google Cloud, as very well as working money for the two, in thousands and thousands of pounds.

TIKR, section results

Services profits just moves greater over time, as it doesn’t look to make a difference what is going on in the overall economy. If look for earnings can survive the malaise that adopted the first COVID outbreak, I basically can not imagine of everything else that could threaten it.

But what about pricing? Very well, that was fantastic as well, with 2020 working income for the phase relocating up 11% in 2020, in the experience of a 100-year pandemic. Final 12 months it was up 68%, and whilst that is certainly unsustainable, it reinforces my point that if you are anxious about a recession’s influence on Alphabet, you are apprehensive about the erroneous issue.

Now, a single possible tailwind that’s coming in the near-expression, other than continued world domination of look for, is the company’s Cloud business. Clearly, Alphabet has been investing very closely in Cloud capabilities, both of those by acquisition and by paying out internally. It has consumed a massive amount of money of money in latest decades, but it is growing strongly, and is near breakeven. We noticed this model with Amazon’s (AMZN) AWS, where by the corporation expended billions of pounds at a decline right up until it attained sufficient scale, and now it’s a big funds cow. Whilst Cloud will not be as critical to Alphabet’s running money as AWS is to Amazon, simply just eradicating this headwind is, in and of by itself, a tailwind.

The issue is that Alphabet being sold off with economically delicate shares, such as advertisers, is rather missing the stage that this corporation isn’t like other advertisers, and as this kind of, should not be treated that way.

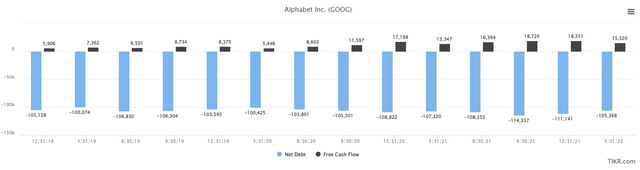

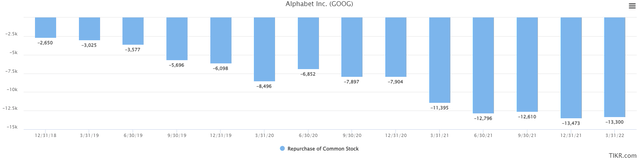

Yet another tailwind is the company’s ample paying on buybacks, which it can do since it has a person of the cleanest balance sheets on the earth.

TIKR, web personal debt and FCF

Web money has been above $100 billion for several years, and remains as these nowadays. But as we can see, the business is also producing $15 billion to $18 billion in new web funds for every quarter, which it is mainly investing on share repurchases. Although that may not appear to be like much in the context of a $1.6 trillion industry cap, it indicates there is a regular consumer of the stock, and in big portions. In addition, it steadily lessens the share depend more than time, juicing EPS by using a decreased float.

Here is what it appears to be like like in follow.

TIKR, share repurchases

Bear in mind these are quarterly figures, so Alphabet is buying roughly $200 million of its individual stock just about every trading day at the instant. Not negative.

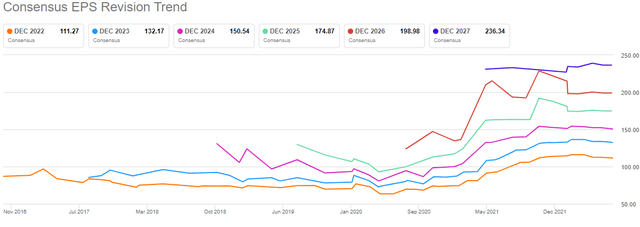

This all boils down to EPS projections, and we can see they have a identical trajectory to profits. When you may well expect that given Alphabet’s superior margins, the share rate is not behaving like EPS is intact.

Trying to find Alpha, EPS revisions

The minimal downward revisions are significantly lesser than what the share price tag has priced in, and which is wherever the prospect is these days. I will not read through the chart to you, but the level below is that estimates proceed to go up and to the remaining, and there is enough space concerning the years, indicating robust expansion more than time. What more could you want?

How about a low-priced valuation?

We have that as nicely with Alphabet, as the inventory has been punished also seriously for true disorders. Under we have cost to modified ahead earnings for the previous 5 several years to give us some context on the existing valuation.

TIKR, ahead P/E

It’s really evident what is occurring below, which is that Alphabet is really just as low-priced as it was through the worst of the COVID providing 2+ several years ago. It traded for ~26X earnings pre-COVID, and ~30X just after COVID, but is 21X now. There is just no way to reconcile that, and it means the stock is far also affordable. For a organization that continues to grow at substantial-teens prices each individual year, and pretty much has what amounts to a monopoly on a company billions of folks use on a everyday foundation, this valuation is just begging to be bought.

Could the setting for advertising deteriorate even further? Positive, anything at all is attainable. But you have to ask by yourself if a valuation that is equal to that of the worst of the COVID marketing makes feeling when we’re not experiencing a new pandemic and the uncertainty that delivers. It seems basic to me that Alphabet has turn into considerably much too low-cost, and that after it breaks out from the consolidation famous previously mentioned, we could simply be off to the races to at the very least 25X forward earnings. That would be ~20% bigger from here, and that seems to me to be just the start.